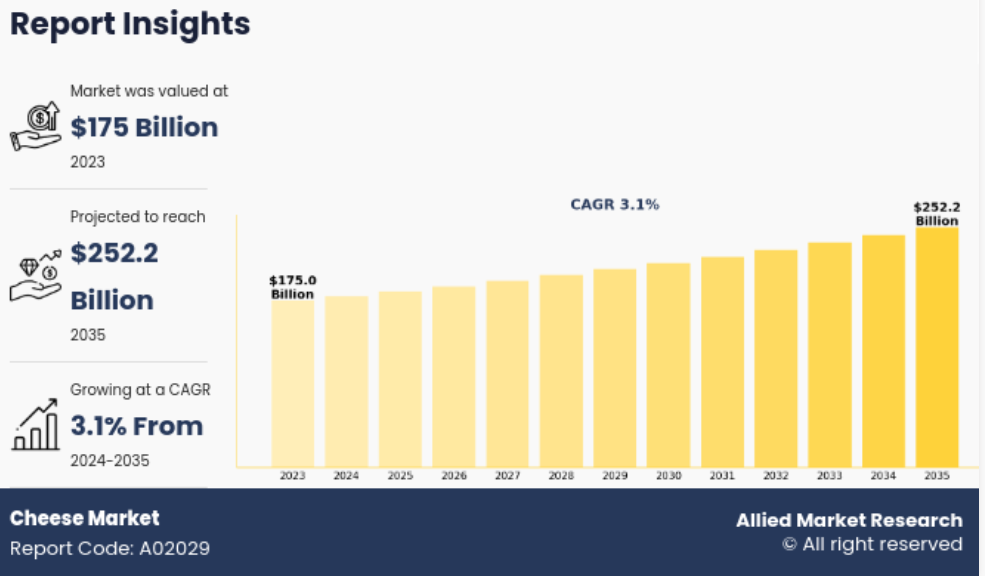

The Global Cheese Market Could Grow to $252.2 Billion by 2035

In 2023, Europe remained the key region in terms of revenue. Its position is attributed to a well-developed cheese-making culture, high per capita consumption, a strong production base, and a wide range of traditional and specialty cheeses. At the same time, the highest growth rates during the forecast period are expected in the Asia-Pacific region, where demand is supported by urbanization, rising incomes, development of food service networks, and the spread of Western dietary habits.

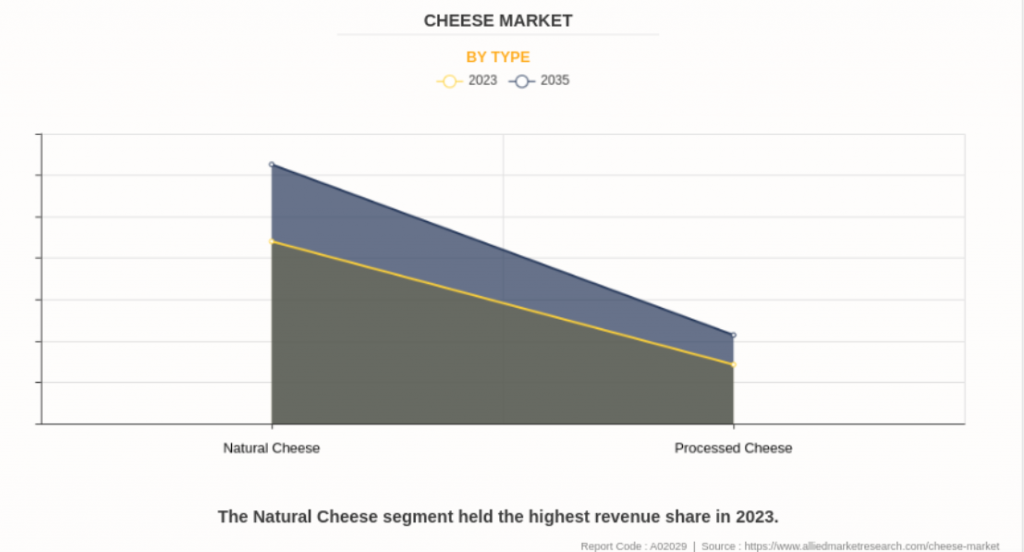

The market structure by product type in 2023 was led by the natural cheese segment. Its growth is supported by the demand for products with more understandable ingredients, as well as consumer interest in authentic flavors and minimally processed dairy products. The processed cheese segment remains important for fast food restaurants, institutional catering, and the mass market, where quality consistency, price, and product technology are critical.

By raw material source, cow's milk cheese holds a dominant position. This segment forms the foundation of the global cheese market due to the availability of raw materials, scale of production, and versatility of cow's milk for producing various types of cheese. Sheep, goat, and buffalo milk cheeses are developing primarily in the premium and specialty segments.

In terms of product categories, cheddar held the largest share in 2023. Its position is explained by its widespread use in home cooking, foodservice, ready meals, burgers, sandwiches, and baking. There is also a high demand for mozzarella, feta, cream cheese, parmesan, gouda, ricotta, mascarpone, and blue cheeses. Mozzarella remains one of the most promising products due to the growing consumption of pizza and the development of food service networks in developing countries.

One of the main drivers of the market is the global development of the food service industry. Restaurants, cafes, fast-food chains, delivery services, and catering companies are increasingly incorporating cheese into their menus—from pizza, burgers, and pasta to salads, baking, and ready meals. This creates demand from producers for consistent quality products with specified melting, flavor, and texture characteristics.

A second significant growth direction is the use of cheese in snacks, baked goods, and fusion cuisine dishes. Cheese is increasingly used in ready-to-eat snacks, baking fillings, savory snacks, and quick-consumption products. This trend is particularly noticeable among urban consumers who prioritize convenience, rich flavor, and new gastronomic formats.

Product innovation holds special importance for the market. Producers are developing lines of plant-based cheese alternatives, products with reduced fat and salt content, lactose-free, high-protein, and fortified options. There is growing interest in cheeses with functional additives, including probiotics, omega-3, vitamin D, and calcium. Such solutions allow companies to engage with audiences that focus on health, convenience, and individual dietary preferences.

However, the market faces several constraints. One of the key pressure factors remains the volatility of raw milk prices and the instability of its availability. Seasonality, feed costs, animal diseases, climatic factors, and logistical disruptions directly affect cheese production costs and processor margins. Smaller producers, in particular, remain vulnerable, as fluctuations in milk prices can lead to a reassessment of production volumes.

An additional challenge is the growing consumer attention to healthy eating. In some countries, part of the audience limits cheese consumption due to its saturated fat and salt content. This encourages producers to develop more balanced recipes and promote products with an improved nutritional profile.

In the competitive environment, key players in the global market remain Arla Foods, Bel Group, Fonterra, Kraft Heinz, Groupe Lactalis, Savencia, Britannia Industries, Associated Milk Producers, Saputo, and Gujarat Cooperative Milk Marketing Federation. Companies employ various growth strategies, including launching new products, developing partnerships, digitalizing sales, expanding geographic presence, and working with sustainable packaging.

The market's prospects will largely depend on producers' ability to combine traditional cheese categories with innovative formats. Premium and artisanal cheeses, products with verified origins, functional cheeses, and plant-based alternatives will intensify competition for consumers. Simultaneously, the development of e-commerce, subscription services, and direct online sales could change the distribution structure, especially in the B2C segment.