Russian Beef Market: Decline in Cattle Numbers and Rising Prices Increase Import Dependency

Beef Cattle Breeding Lags Behind Dairy Production

The livestock industry in Russia is still predominantly focused on dairy production, while the beef sector is in its formative stage.

In 2025, the structure of beef production was as follows:

- household farms — 46%

- agricultural enterprises — 41%

- farmer-owned enterprises — 13%

A significant portion of beef production comes fr om the culling of dairy herds, which limits the development of a specialized beef segment.

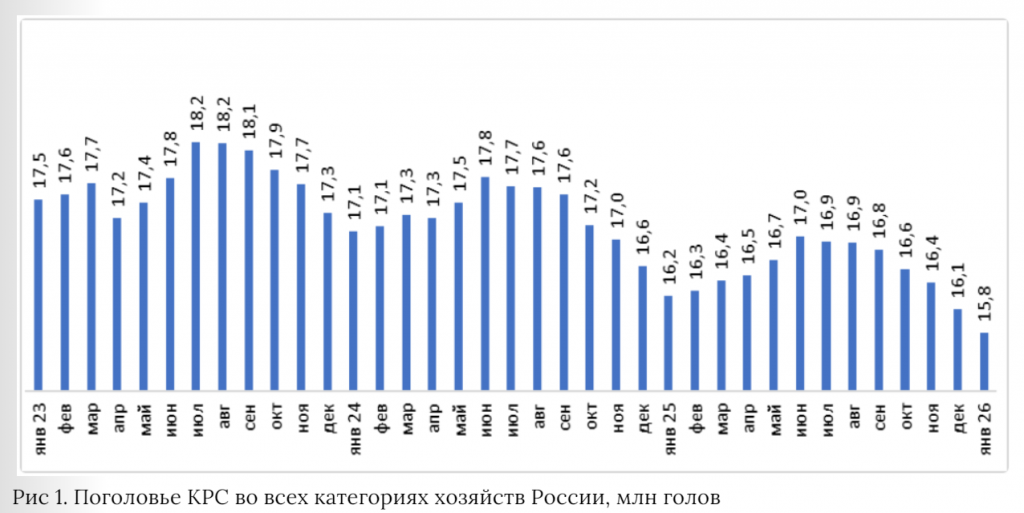

Cattle Numbers Continue to Decline

The key negative factor is the persistent decline in livestock numbers:

- total cattle — 15.8 million (-2.9% year-on-year)

- cows — 7.3 million (-3.6%)

The decline occurs mainly in household farms, while the organized sector shows more stable dynamics.

Beef Production Declines

By the end of 2025:

- production — 1.566 million tons (-4.6%)

- share in total meat production — 13%

For comparison:

- poultry — 46%

- pork — 39%

A decline was recorded in all farm categories, including the industrial segment.

Regional Structure: Dominance of the Center and Volga Regions

Main production areas:

- Volga Region — 27%

- Central Federal District — 20%

- Southern Russia — 16%

The Central region leads in the industrial segment (38%), wh ere large players like Miratorg are concentrated.

Price Growth Becomes a Stable Trend

Amidst reduced supply and rising costs:

- beef prices show a steady increase

- wholesale price — 466.8 RUB/kg (+8.6% year-on-year)

Beef remains one of the most expensive types of meat for consumers.

Imports Maintain a Key Role

Despite industry development, Russia remains dependent on external supplies:

- imports — about 50% of domestic production in the industrial segment

Main suppliers:

- Brazil

- Belarus

- India (rapidly increasing share)

Beef exports remain limited:

- 33.3 thousand tons in 2025

- main market — China

Feed Base: Stability with Weak Growth

The feed segment shows relative stability:

- compound feeds — 82% of feed production

- feed output for cattle — 3.16 million tons (+0.8%)

The structure is mainly oriented towards poultry and pig farming.

Strategic Industry Constraints

The Russian beef market is shaped by systemic factors:

- decline in cattle numbers

- high production costs

- long payback periods

- investment shortage

- limited domestic demand

Industry estimates indicate that achieving self-sufficiency requires increasing the cattle population by 4 million.