Russian Dairy Market Increases Production by 4% in 2024, Volume May Reach 31.3 Million Tons by 2030

According to the Business Profile Group, despite the overall growth in milk production, there remains a high dependency on imported technologies and fluctuations in production costs. In 2024, producer costs grew faster than retail prices, putting pressure on profitability and increasing the need for modernization.

Production and Market Structure

According to Soyuzmoloko, a price disparity was observed in 2024: the cost of raw milk increased by 28.8%, finished products by 26.7%, while retail prices rose by only 15.7%. With inflation at 11.4% and rising feed (+49%) and electricity (+11%) costs, producer profitability remained limited.

Production growth was uneven: the Volga Federal District increased volumes by 6.6%, while Leningrad and Novosibirsk regions saw a decline of 2% to 7% due to climatic and economic factors.

The leading regions in commercial milk volumes were:

-

Novosibirsk Region — 1.486 million tons;

-

Moscow Region — 1.221 million tons;

-

Republic of Tatarstan — 1.200 million tons.

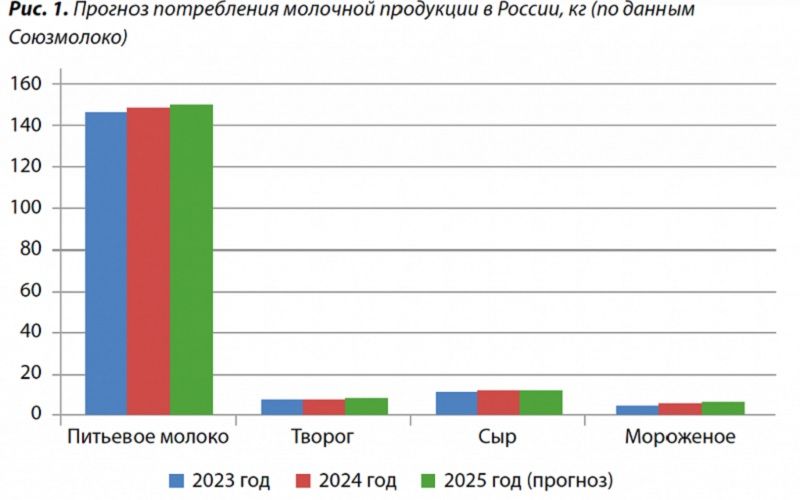

Domestic demand for dairy products grew by 3%, with ice cream sales (+17%), cream (+13.6%), and yogurts (+9.1%) driving growth. Demand for cheese and kefir decreased by 1% and 0.4% respectively.

Consumption and Changing Demand Structure

Consumer preferences are shifting towards functional and vitamin-enriched products. According to Nielsen, the segment of functional yogurts grew by 14-17%, and plant-based milk alternatives accounted for 5% of the market, primarily in large cities.

At the same time, traditional categories — drinking milk, cottage cheese, and kefir — maintain a high share but show slowing growth.

The self-sufficiency level of Russia in milk is:

-

drinking milk — 147%,

-

cottage cheese — 101%,

-

butter — 85%,

-

cheeses — 76%.

The lack of domestic raw materials for cheese and butter production remains a key limitation in processing development.

Government Support and Regulation

The dairy industry remains one of the priority areas of the state's agricultural policy. In 2025, concessional loans at 8.3% per annum, feed subsidies, and livestock insurance through the FGIS "VetIS" system remain in effect.

From September 1, 2025, new rules for organic product labeling will take effect: only certified producers will be allowed to use the terms "bio" and "eco". This will create new transparency standards in the market but will increase entry barriers.

An important anti-crisis measure was the temporary abolition of duties on butter imports (up to 25 thousand tons from December 2024 to June 2025), which stabilized the fat market amid shortages.

Cost and Technological Dependency

In 2024, the average cost of raw milk increased by nearly a third, and processing costs rose by 26-27%.

Main factors of cost increase:

-

compound feed — +49%,

-

electricity — +11%,

-

labor costs — +20%.

About 70% of the technological equipment for processing and cheese-making is still imported. Dependency on foreign solutions hinders localization and increases currency risks. In these conditions, the industry focuses on developing domestic engineering analogs and energy-efficient solutions.

Impact of Demography and Climate

Demographic decline is a key restraining factor for domestic demand. Russia's population is decreasing by 0.3-0.5% annually, and the share of citizens over 60 years old has exceeded 20%, limiting dairy product consumption.

Climate changes also increase risks. Droughts in southern regions (2020, 2022, 2024) reduced the yield of forage crops, leading to higher feed prices. In response, projects on irrigation, feed storage, and the implementation of drought-resistant grasses are prioritized.

Technology and Modernization

The industry is rapidly implementing automation and digital solutions:

-

automatic milking and animal health monitoring systems;

-

IoT platforms for farm management;

-

energy-efficient processing technologies;

-

biotechnology use to increase productivity.

Modernization allows for an annual increase in milk yield by 4-5%, reduces costs, and improves milk quality.

Foreign Trade and Export Potential

Dairy product exports are growing at an outpacing rate. In 2024, exports amounted to 0.78 million tons, expected to reach 1.1 million tons in 2025, and 1.5 million tons by 2030.

Main destinations are Central Asia, the Middle East, China, India, and Southeast Asian countries.

Imports, on the other hand, decreased to 5.3 million tons and are forecasted to decline to 4.1 million tons by 2030. Increasing export volumes and reducing import dependency will be key indicators of the industry's sustainability.

Forecast to 2030

Experts estimate that the volume of commercial milk production in Russia will continue to grow at a moderate pace:

-

2025 — 26.8 million tons,

-

2030 — 31.3 million tons (+19% to 2024).

Growth will be ensured by increased productivity, the construction of new dairy farms, and government support.

Per capita consumption will remain at 330-340 kg per year, but its structure will change — the share of functional and lactose-free products will increase, while consumption of traditional categories will decrease.

Retail prices will continue to rise: with base inflation of 4-5%, the average price of drinking milk may reach 85-90 rubles/liter by 2030, and exceed 100 rubles/liter with stress inflation of 7-8%.

Strategic Directions

Experts note that sustainable market development is possible under three conditions:

-

Increasing production efficiency — development of domestic feeds, energy saving, digital accounting implementation.

-

Expanding exports — market diversification and brand promotion under the "Natural and Safe Origin" label.

-

Supporting SMEs — restoring concessional lending up to 70% of the key rate for farmers and regions with milk shortages.