The Global Milk Market: From Weakness to Cautious Optimism

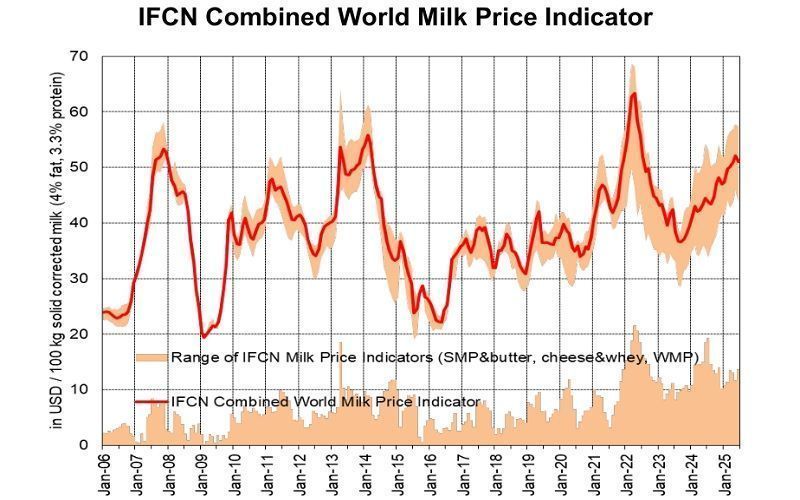

The global milk price remains under pressure, yet the market is showing early signs of stabilization. According to IFCN's June 2025 data, the Combined World Milk Price Indicator decreased by 2.2%, reaching 51.0 USD per 100 kg of standardised corrected milk (SCM). This figure reflects market nervousness, though it remains within recent months' range.

The price decline is primarily driven by falling quotations for cheese and whole milk powder (WMP), a consequence of both seasonal factors and structural imbalances in certain regions. Nevertheless, global milk production is recovering, with growth particularly evident a month after the spring flush.

"Global demand remains firm, despite a slight decline in the powder market," IFCN analysts report. However, the outlook is mixed. Futures markets project milk prices ranging between 46 and 57 USD per 100 kg SCM throughout 2025, with widening regional disparities.

In New Zealand, a key dairy exporter, average prices dropped by 5% to 52 USD, driven by concerns over drought conditions on the North Island. Meanwhile, prices in the EU rose by 1.5% to 57 USD, and in the US by 3.7% to 48 USD, bringing American price levels close to those in Oceania.

Future market dynamics will depend on production growth under favourable weather conditions, uncertainty over China’s import volumes, and ongoing trade risks. A "fight for milk" is particularly evident in Europe, where persistent raw milk shortages keep prices elevated. At the same time, the strengthening US dollar against the euro reshapes trade flows.

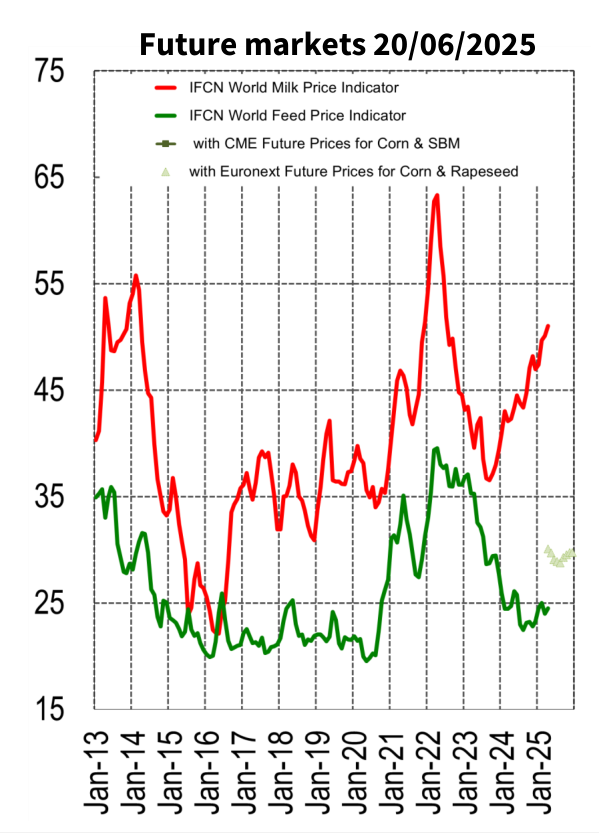

While global milk supply shows signs of improvement, farmers continue to face volatile production costs. World feed prices have fallen to 23.1 USD per 100 kg (-2.5% month-on-month), supported by higher corn harvests in India and increased exports from the US and Canada. Yet, weather risks in North America and the geopolitical fallout from Middle East tensions continue to cloud the outlook.

Overall, the global milk market is cautiously moving towards recovery. But significant regional price gaps and geopolitical uncertainties keep the industry's future unpredictable.

"Global demand remains firm, despite a slight decline in the powder market," IFCN analysts report. However, the outlook is mixed. Futures markets project milk prices ranging between 46 and 57 USD per 100 kg SCM throughout 2025, with widening regional disparities.

In New Zealand, a key dairy exporter, average prices dropped by 5% to 52 USD, driven by concerns over drought conditions on the North Island. Meanwhile, prices in the EU rose by 1.5% to 57 USD, and in the US by 3.7% to 48 USD, bringing American price levels close to those in Oceania.

Future market dynamics will depend on production growth under favourable weather conditions, uncertainty over China’s import volumes, and ongoing trade risks. A "fight for milk" is particularly evident in Europe, where persistent raw milk shortages keep prices elevated. At the same time, the strengthening US dollar against the euro reshapes trade flows.

While global milk supply shows signs of improvement, farmers continue to face volatile production costs. World feed prices have fallen to 23.1 USD per 100 kg (-2.5% month-on-month), supported by higher corn harvests in India and increased exports from the US and Canada. Yet, weather risks in North America and the geopolitical fallout from Middle East tensions continue to cloud the outlook.

Overall, the global milk market is cautiously moving towards recovery. But significant regional price gaps and geopolitical uncertainties keep the industry's future unpredictable.

Key News of the Week