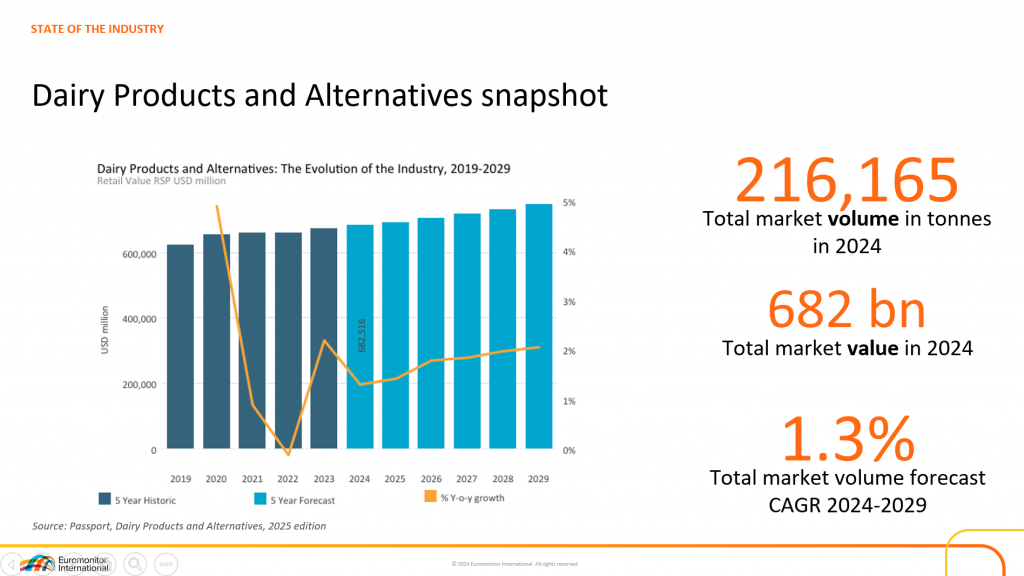

Global Dairy Market Stabilizes as E-commerce, Private Labels, and Emerging Markets Drive Growth

Cheese remains the top-performing category in terms of value growth, largely driven by rising consumption in Asia. Drinking milk continues to see solid demand in developing countries, while plant-based alternatives, though still a niche in terms of market share, are expanding at the fastest pace with double-digit growth rates.

India and other Asian countries are emerging as new global consumption powerhouses. India is expected to lead volume growth by 2029, fueled by urbanization and a shift fr om unpackaged to packaged dairy products. The United States follows closely, driven by growing cheese demand. Long-term demand will also be shaped by countries in Africa and Southeast Asia, wh ere demographic trends and evolving consumption patterns are creating sustained growth opportunities.

Retail dynamics are also shifting, with e-commerce now the fastest-growing sales channel across all regions. At the same time, private label brands are gaining consumer trust by offering accessible prices and enhanced functionality. The market share of private labels rose from 12.8% in 2019 to 14.9% in 2024, with notable growth in drinking milk and dairy snack segments.

In the Middle East and North Africa (MENA), the dairy market grew by 5% in 2024, with a forecasted CAGR of 4% through 2029. The region’s market value stands at $65 billion, supported by easing inflation and increased investment in modern retail infrastructure—particularly in Saudi Arabia under its Vision 2030 program. While modern retail chains dominate, traditional grocery formats remain relevant in parts of Africa. Retailers such as Viva in the UAE exemplify the rise of discount formats focused on high-quality European private label offerings.

Five major trends are shaping consumer behavior in the dairy industry. First, health has become a central focus, with growing interest in products supporting digestion, immunity, and protein intake, as well as vitamins D and B6. Examples include Danone’s Activia Mix&Go with probiotics, Actimel+ for immune support, and Estonia’s TERE Fit!, a sugar-free, high-protein yogurt designed for on-the-go consumption.

Second, consumers are increasingly opting for snackable dairy formats, such as Arla’s Protein Food to Go, which serves as a meal replacement. Third, plant-based alternatives continue gaining ground, driven by health, sustainability, and animal welfare concerns. Australian brand PlantWell, for example, offers soy, oat, and almond-based drinks targeting bone health, cholesterol reduction, and immune support.

Fourth, private label products that combine affordability with functional benefits are on the rise. SPORT by Leclerc (France), a premium store brand with high protein content, highlights this trend. Finally, sustainability and local sourcing are becoming decisive factors for consumers, with two-thirds preferring products with a smaller environmental footprint and local origin. Brands that support local communities and promote shorter supply chains are seeing increased loyalty.

According to Monique Naval, Global Project Leader at Euromonitor International, traditional dairy will maintain its strong position, especially in developing markets, while plant-based alternatives will continue to gain share, intensifying market competition. “The future belongs to brands that thoughtfully combine functionality, sustainability, and lifestyle adaptation,” Naval concluded.

Gold Partners

- Al Ain Farms Group

- Imperial

Innovation Partners

Partners